Central banks and fintech companies now shape the same financial segments. Their roles differ, but their actions increasingly intersect. Central banks set the rules, guard stability, and manage money. Fintech firms design products, build infrastructure, and change how financial services are delivered. Understanding how these forces interact is essential for anyone analysing modern finance.

Why central banks care about fintech

Fintech innovation affects payments, lending, savings, and capital markets. These areas sit at the heart of monetary and financial stability. When new technologies scale quickly, central banks must assess their impact on risk, inclusion, and trust in money.

Three drivers explain the growing focus on fintech.

First, technology changes how money moves. Real-time payments, digital wallets, and APIs reduce friction but also increase speed and interconnectedness. Faster systems can amplify shocks if not well designed.

Second, non-bank actors now perform functions once dominated by banks. Payment firms, neobanks, and crypto platforms handle large transaction volumes without traditional balance sheets. This challenges existing supervisory models.

Third, public expectations have shifted. Consumers compare financial services to technology platforms. Central banks face pressure to ensure that safety and efficiency keep pace with user experience.

Regulatory innovation and supervisory technology

Central banks no longer rely only on static regulation. Many now experiment with new tools to supervise fast-moving markets.

Regulatory sandboxes allow fintech firms to test products under controlled conditions. These initiatives help supervisors understand new business models while reducing uncertainty for innovators. They also signal regulatory openness, which can attract investment.

Supervisory technology, often called SupTech, uses data analytics, machine learning, and automation to improve oversight. Instead of periodic reporting, supervisors can analyse near real-time data. This shift improves risk detection and reduces compliance costs.

Institutions such as the Bank for International Settlements have played a coordinating role, sharing best practices and supporting cross-border learning.

Payments infrastructure as a strategic priority

Payments are the most visible intersection between central banks and fintech. Instant payment systems now exist in many jurisdictions, often operated or overseen by central banks.

These systems provide a public backbone on which private firms build services. Fintech companies add user-friendly interfaces, value-added services, and cross-border features. Central banks ensure resilience, interoperability, and fairness of access.

Open banking strengthens this dynamic. By mandating data sharing through secure APIs, regulators reduce barriers to entry while maintaining consumer protection. Central banks support these frameworks because they enhance competition without undermining stability.

CBDCs

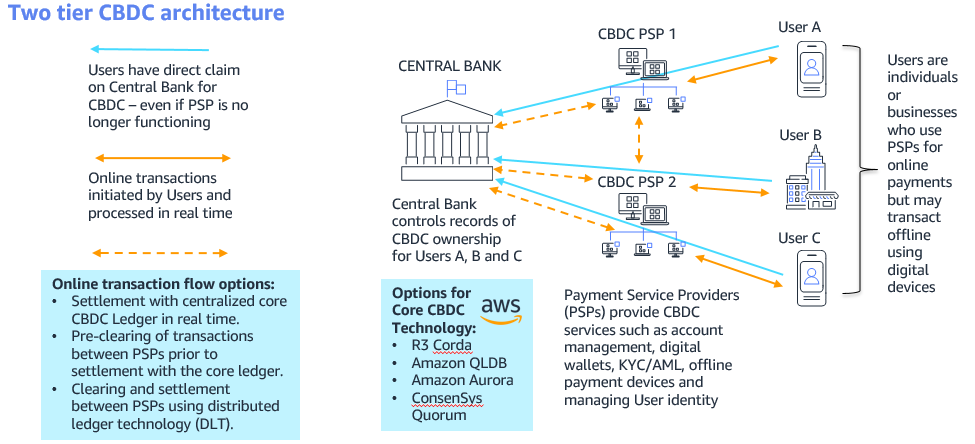

Central bank digital currencies, or CBDCs, represent the most direct engagement between central banks and financial technology.

A CBDC is a digital form of central bank money, distinct from bank deposits or private stablecoins. Motivations differ by country but often include payment efficiency, financial inclusion, and monetary sovereignty.

Fintech firms play several roles in CBDC projects. They build wallets, design user interfaces, develop compliance tools, and test scalability. Central banks define the core architecture, governance, and legal framework.

The European debate illustrates this balance. The European Central Bank explores a digital euro while emphasising privacy, intermediated distribution, and coexistence with private innovation.

Managing risks without stifling innovation

Central banks face a delicate trade-off. Overregulation can slow innovation and entrench incumbents. Underregulation can create systemic risks and erode trust.

Key risk areas include operational resilience, cyber security, data protection, and concentration risk. Cloud dependence and third-party providers require particular attention, as failures can cascade across institutions.

To manage this, many central banks favour activity-based regulation. The focus is on what a firm does, not what it is called. If a fintech provides payment services at scale, it should meet similar standards to other payment providers.

Dialogue matters as much as rules. Regular engagement with fintech firms helps supervisors anticipate risks rather than react to crises.

The geopolitical dimension

Fintech and central banking also intersect at a geopolitical level. Cross-border payments, sanctions enforcement, and currency competition all have technological components.

CBDCs and faster payment rails could reshape international settlement. Some countries view domestic digital currencies as tools to reduce reliance on foreign payment networks.

Coordination remains essential. Fragmented standards would increase costs and risks. Central banks therefore work through international forums to align principles, even when national priorities differ.

What this means for fintech founders and investors

For fintech companies, central banks are not distant institutions. They shape market access, data standards, and infrastructure choices.

Founders should understand central bank priorities early. Products aligned with resilience, transparency, and inclusion face fewer regulatory surprises. Investors increasingly assess regulatory exposure alongside product-market fit.

For policymakers, fintech is not a side topic. It is part of core monetary and financial policy. The most effective approaches treat innovation as a permanent feature, not a temporary disruption.

Looking ahead

The relationship between central banks and fintech will deepen. Payments will become faster and more programmable. Supervision will become more data-driven. Public and private money will coexist in more complex forms.

Success depends on balance. Central banks must protect trust in the financial system while allowing new models to emerge. Fintech firms must innovate within frameworks designed for long-term stability.

In this shared space, technology is an enabler, not the objective. The real challenge lies in governance, incentives, and execution.