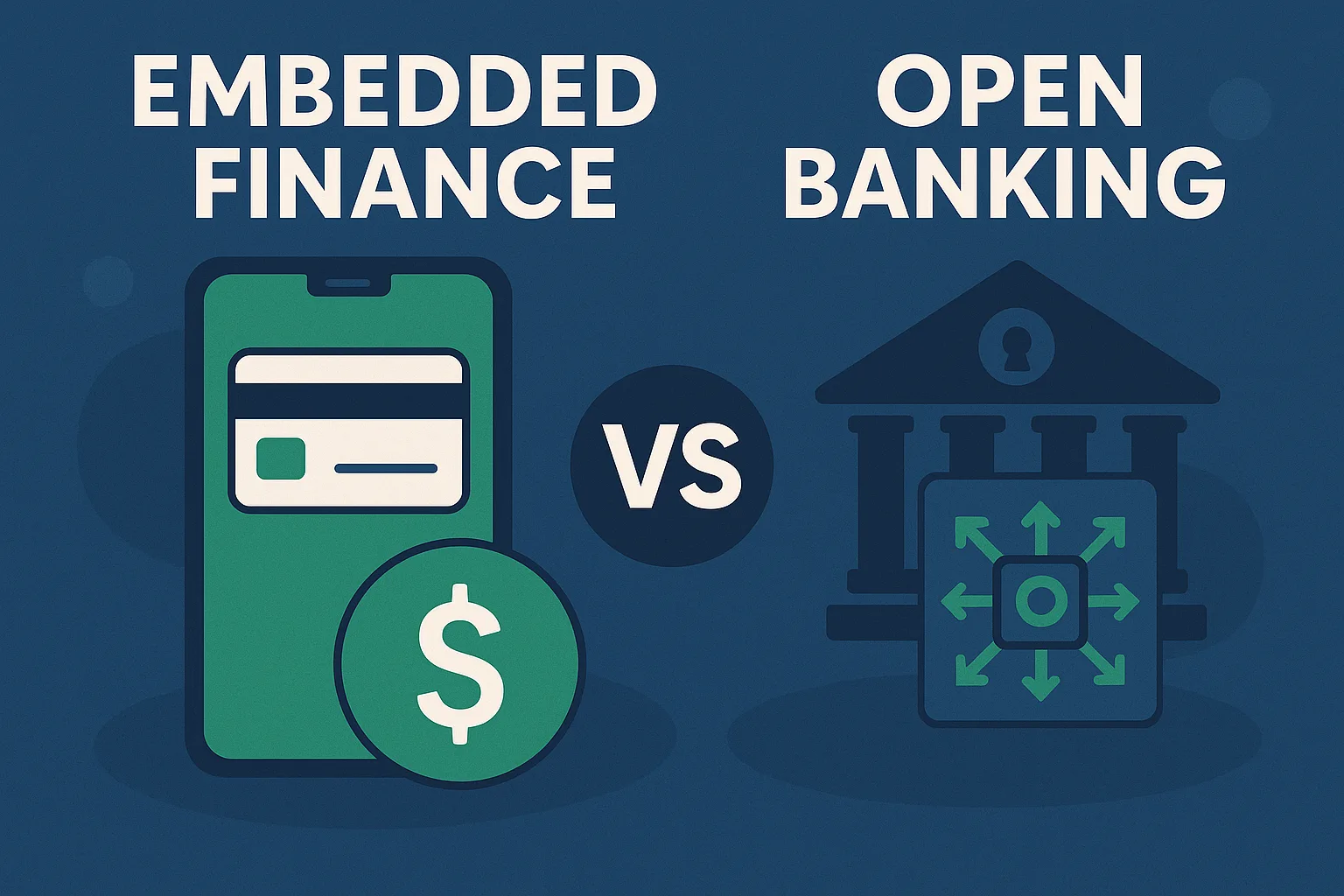

Embedded finance and open banking are often mentioned together, but they serve different functions. Both reshape financial services, yet their business models, target audiences, and monetisation approaches diverge sharply.

Embedded finance integrates financial services into non-financial platforms. For example, a ride-sharing app offering in-app payments or lending options. Open banking allows third-party providers to access banking data through APIs, enabling customers to share their financial information securely across services. While both rely on API infrastructure, embedded finance focuses on embedding services directly into customer experiences, whereas open banking centres on data portability and customer empowerment.

Revenue generation and customer experience

Embedded finance platforms earn revenue directly from services they embed. They capture transaction fees, loan interest, insurance commissions, and SaaS subscription fees. Open banking providers typically monetise through API access fees, partnerships, consulting services, or value-added products built on open banking data. In some markets, open banking providers generate revenue by enabling financial institutions to comply with regulatory mandates while developing innovative use cases for consumers and businesses.

Embedded finance prioritises seamless customer journeys. Financial products are offered contextually where users already engage. This reduces friction and increases adoption rates. Open banking empowers users by giving them control over their financial data and enables new personal finance, budgeting, and aggregation tools. Open banking applications often focus on transparency, helping users compare products, optimise savings, and improve financial decision-making.

Speed of adoption

Embedded finance often operates under banking-as-a-service partnerships, requiring collaboration with licensed institutions. Regulatory compliance is delegated through these partnerships. Open banking is governed by specific regulations like PSD2 in Europe, mandating banks to open access to customer data with consent. Open banking frameworks typically require higher standards of data security, consent management, and transparency, while embedded finance may navigate more complex regulatory licensing via partnerships.

Embedded finance has grown rapidly, fuelled by non-financial brands integrating financial products to enhance user loyalty. Open banking adoption has been steadier, driven by regulatory deadlines and varying levels of consumer awareness and trust. Embedded finance benefits from immediate business incentives, while open banking often depends on longer-term shifts in consumer behaviour and regulatory pressure.

Technology stack and use case examples

Embedded finance relies on Banking-as-a-Service (BaaS) platforms, card issuing services, embedded lending providers, and insurance partners. Open banking depends on secure API standards, strong authentication protocols, data aggregation platforms, and consent frameworks. Many open banking platforms also invest heavily in analytics and machine learning to deliver actionable insights from raw financial data.

An online marketplace offering point-of-sale financing exemplifies embedded finance. A personal finance app aggregating multiple bank accounts demonstrates open banking. Some companies combine both, using open banking data to power embedded finance offers, such as personalised credit scoring or insurance underwriting based on live banking data.

Strategic considerations

Businesses choosing between embedded finance and open banking should assess their control needs, regulatory obligations, technological capabilities, and monetisation goals. Embedded finance allows deeper customer integration, driving retention and revenue per user. Open banking enables broad data-driven innovation, often opening new competitive landscapes for fintech providers and legacy banks alike.

Embedded finance and open banking complement each other but serve distinct purposes. Embedded finance focuses on delivering financial services within existing user journeys. Open banking unlocks customer data to drive new financial solutions. Both offer diverse monetisation opportunities depending on the business model. In practice, many forward-looking fintech companies are beginning to blend both approaches to maximise customer value and competitive advantage.