As financial technology reshapes the global economy, two concepts often used interchangeably are in fact quite distinct: Banking-as-a-Service (BaaS) and Embedded Finance. While both contribute to the democratisation of financial services and enable non-banks to offer financial products, their roles in the fintech ecosystem are different. Understanding the distinction is essential for startups, banks, and investors navigating this rapidly evolving space.

Defining Banking-as-a-Service (BaaS)

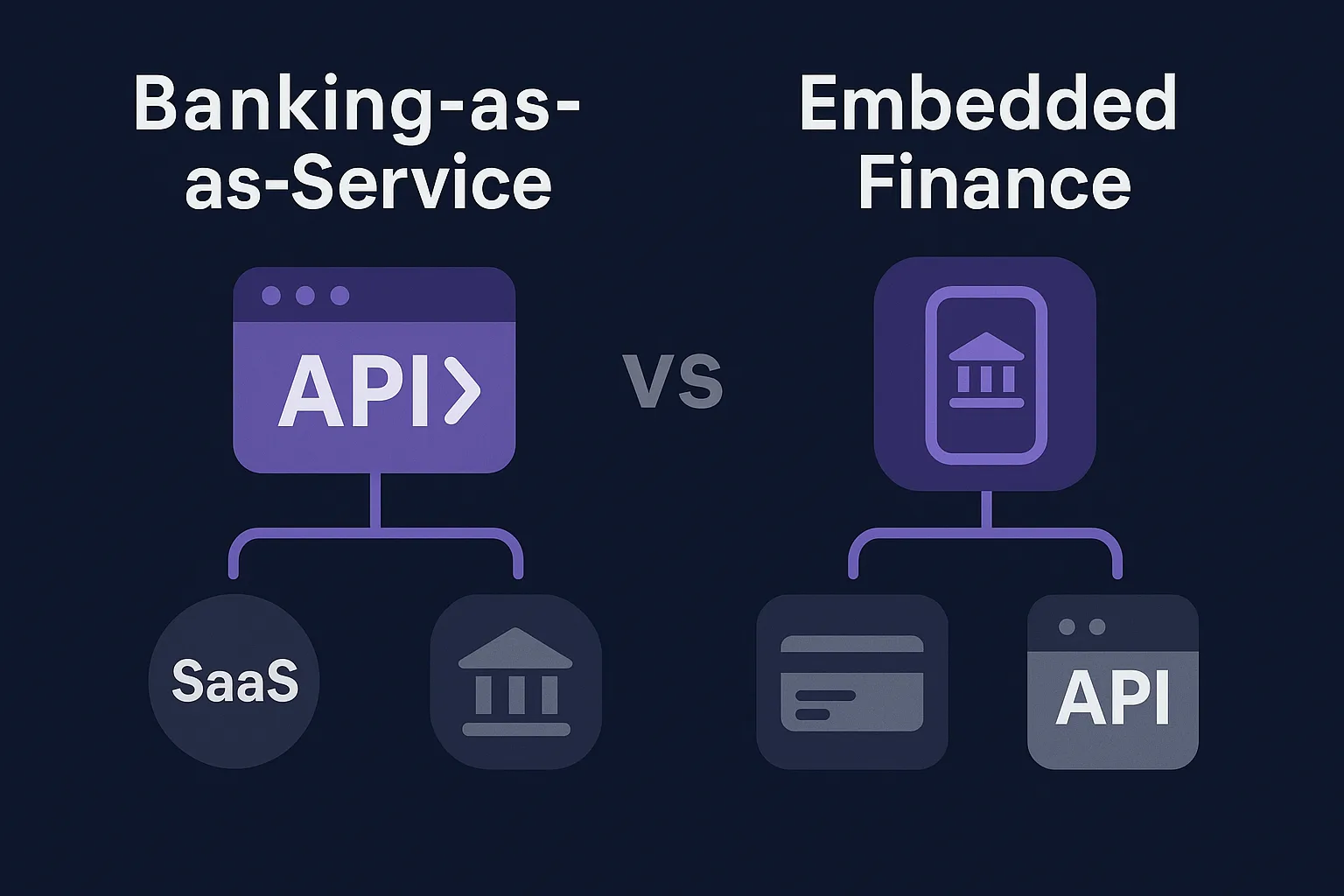

Banking-as-a-Service refers to the provision of banking infrastructure via APIs, allowing third parties to build financial products on top of licensed banking platforms. In essence, BaaS providers enable fintechs, neobanks, and non-financial firms to offer regulated financial services. Without holding a banking licence themselves.

These services include:

- Account creation and management

- Payments and money transfers

- Debit and credit cards

- Lending and savings products

- Regulatory compliance (KYC, AML)

BaaS platforms act as the infrastructure layer, offering a modular suite of plug-and-play banking functions. Common providers include Solaris, Treezor or the now-defunct Synapse (US).

Understanding Embedded Finance

Embedded finance, on the other hand, is a broader trend referring to the integration of financial services within non-financial products. It enables companies such as retailers, marketplaces, or SaaS platforms to embed payments, lending, insurance, or banking directly into their customer journeys.

Examples include:

- A ride-sharing app offering a driver debit card

- A B2B SaaS platform providing instant invoice financing

- An e-commerce site enabling buy-now-pay-later at checkout

- A marketplace integrating wallet functionality for sellers

Embedded finance is focused on user experience and distribution, not infrastructure. It is the “frontend layer” of fintech, where finance becomes invisible but deeply integrated into daily digital services.

Key Differences Between BaaS and Embedded Finance

BaaS is the toolkit, embedded finance is the application. BaaS enables companies to build financial products. Embedded finance enables them to offer those products within their own services.

How They Work Together

Rather than being in competition, BaaS and embedded finance are complementary layers of the fintech stack.

For instance:

- A retail platform like Shopify offers Shopify Balance accounts to its merchants. This is embedded finance.

- Behind the scenes, Shopify partners with a BaaS provider (such as Stripe Treasury) to power those accounts. This is BaaS.

The embedded experience is consumer-facing, while BaaS powers it quietly in the background. In many cases, multiple BaaS providers work together to handle card issuance, compliance, and payments.

Why the Distinction Matters

Understanding the difference between BaaS and embedded finance is crucial for several reasons:

- Business Models: BaaS providers typically charge platform fees or volume-based pricing. Embedded finance players monetise via customer engagement or financial margins.

- Regulatory Impact: BaaS operators must meet regulatory requirements or partner with licensed institutions. Embedded finance providers focus on UX and rely on partners for compliance.

- Market Strategy: Startups must decide whether to build with BaaS or embed finance into their own offer. The decision impacts tech architecture, licensing needs, and revenue models.

- Investor Clarity: Investors need to understand where a company sits in the value chain: are they providing the rails, or building the experience?

Conclusion

Banking-as-a-Service and embedded finance are two sides of the same fintech coin. BaaS provides the critical infrastructure, while embedded finance brings it to life in everyday apps and services. As financial services continue to decentralise, expect tighter integration between these layers. More companies will blur the lines between builder and distributor.

Whether you’re building a new neobank or embedding payments into your e-commerce platform, knowing the distinction can help you choose the right partners, architecture, and strategy.

: The Future of Financial Services?")