Fintech is changing financial services for the better. That is the mantra. Or at least, it is supposed to… That is what everybody was and is still expecting. The fintech wave, that great innovation movement that notably happened after the financial crisis of 2008 is built on many promises. One of its strongest promises, though, is that it is going to build a more inclusive financial services industry. Notably by including many more women than before. And yet, it seems that it is not at all perfect- Far from it. Particularly when it comes to gender balance and equality. Let’s dive in, what is the state of women in fintech today?

“In order for consumers to get the products and services that they need, we need not only to start investing in diverse ideas and founders but also ensure that the people around the table making the investment decisions are diverse. Today, only 2% of venture capital funding goes towards women-founded businesses, and even less than that goes toward women of colour. As an ecosystem, we must work together to create greater access to opportunities and capital for female founders to help drive innovation, new products and services, and an equitable future for all entrepreneurs.”

— Michelle Beyo, CEO of Finovator

“Even if you are optimistic, it is hard to be content about the state of women in fintech today. There is still much to do before we have a truly inclusive industry. Fintech is failing its promise to be better than good old financial services. However, there are plenty of reasons to hope for a brighter future, if we continue to push everybody in the right direction.”

— Tristan Pelloux, Chief Pencil Officer of Fintech Review

How it looks like in Europe, North America and elsewhere…

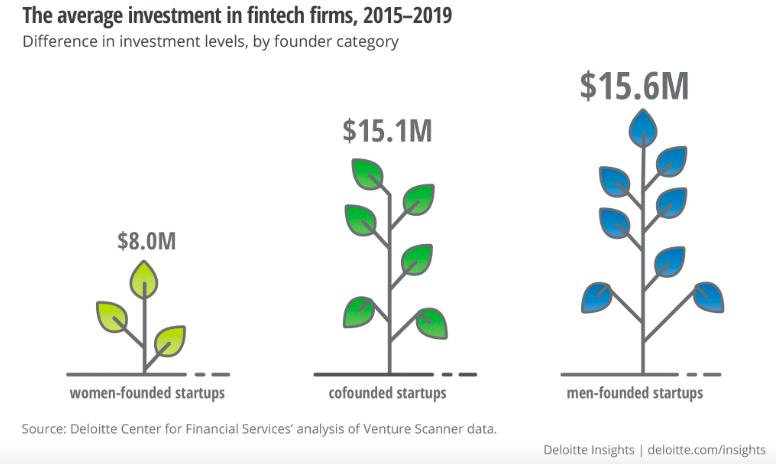

It is obviously not the same in all of the geographies. In some places, it is slightly better than others. That is the good news, let’s say. The bad news is that globally, let’s not sugarcoat it, it is not great at all. Let’s have a brief look at it from a numbers’ perspective: only 1.5% of global fintech firms are founded solely by women. These companies receive just over 1% of total fintech funding according to Findexable. There are not a million ways to look at these numbers and think that we are in a satisfactory state.

Women are starting less fintech companies, and getting even less overall funding when they eventually do. Last but not least, women are on average getting less funding per funding round than men-founded startups. It is a man’s man’s world in fintech, it seems. Very much like the old banking system that it is disrupting.

Furthermore, it is quite thin in terms of women in the executive management of fintech companies. The largest proportion of women executives (26%) in the sector are Chief People Officer or Head of HR. That is followed by Chief Marketing Officer (CMO) and Chief Financial Officer (CFO). And of all fintech CEOs globally, 5.6% are women, and less than 4% of women hold the title of Chief Innovation (CIO) or Technology Officer (CTO).

Climbing the pyramid…

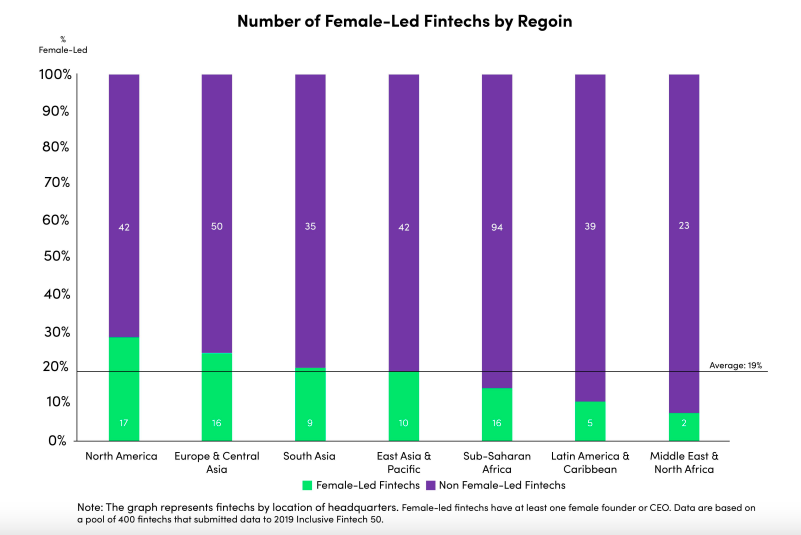

In North America, only 4.8% of company founders are women, compared to 7.7% of women founders in Asia, 7.4% in Africa, and 6.5% in Europe. Therefore, in Europe the proportion of female founders is slightly higher than in the U.S. but it is not something to brag about given how low the numbers are. Silver lining, possibly, North America has the highest proportion of female executive team members. Companies in North America with at least one female founder have historically received the highest median funding as well, given the strength of the venture capital industry in the region. It is not all that doom and gloom.

However, scaling is also an issue: alarmingly, only 8 female-founded companies have more than 1,000 employees. That represents five companies in Asia, two in Europe and just one in Latin America. Europe has 149 top fintechs and only 12 female CEOs. That is quite dire.

In the UK, a mere 17% of fintech companies have female founders. Meanwhile, women account for less than 30% of the sector’s overall workforce, according to Innovate Finance. In addition, women receive just 3% of venture capital funding in the sector. Again, it means that startup investors are less willing to invest in female-led fintech companies.

There are some positive developments…

The current state of women in fintech is far from fantastic. However, there are positive developments that make a lot of people inside and outside the industry think that the situation is improving. And that the future will be much brighter.

There has been some positive movement in the fintech industry and the state of diversity is slowly but surely progressing. Today, 13% of European fintechs have female founders which means that it is better than the overall company creation statistics. There are plenty of top female-founded fintech startups that are taking the European market by storm: Starling Bank, Lovys, Azimo, Mambu, Billie, Molo, PensionBee, Pollinate, Fluidly, or GoHenry, to name a few.

Although it is applying to a broader scope of companies, France passed a law more than 10 years ago to impose gender parity in Boards of Administration and senior management of medium to large listed companies. The French government is also thinking about building on this law to push even further into stronger diversity governance. The EU followed suit recently, announcing that in June 2022 that it is targeting that at least 40% of the underrepresented gender must be represented in non-executive boards of listed companies or 33% among all directors. That is building on the fact that Europe has many highly qualified women with 60% of current university graduates being female.

There is hope that Canada could follow suit as only 17% women are board members right now. The UK is also going in the same direction.

This has a positive impact on the management composition of companies in all sectors including financial services. It forces companies to build a pipeline of future female leaders and to deeply review the way people are hired and promoted.

Going up!

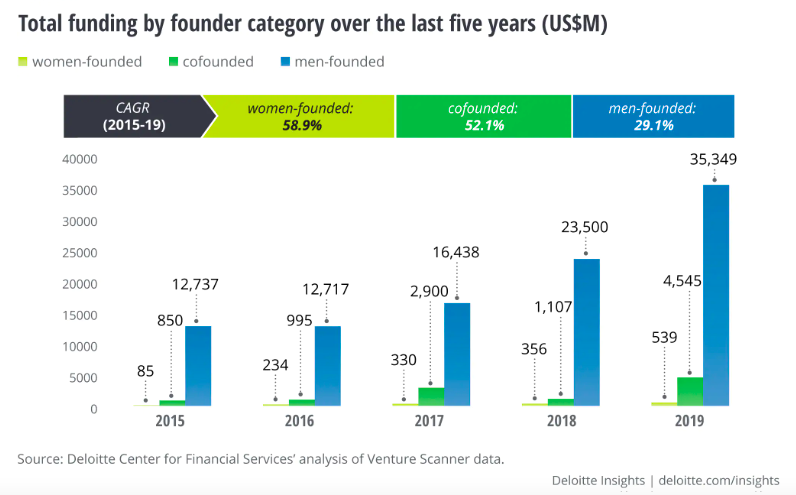

As of 2021, startups founded by women have significantly increased their median valuation. It went from $30 million to $45 million in the last year. Late-stage startups also went up 69% from $70 million to $120 million. The trends for venture capital funding involving women-led fintechs is expected to grow: many of their businesses experienced incredible resilience during the global economic downturn.

Funding for women-founded startups grew at a compound annual growth rate of 59%, while funding for men-founded companies grew by 29.1%. Women fintech leaders bring unique perspectives to the fintech space, experiencing fintech products in a different way than men. Companies with the greatest number of women in top management had a 41% higher return on equity than the average.

For instance, Canada’s Women Entrepreneurship Strategy has positioned the country as a leader when it comes to supporting the launch of female-led businesses, with a goal of doubling the number of female entrepreneurs by 2025.

Federal and provincial governments, as well as private funders, have launched several policies and programs centred around helping women finance, grow and scale their businesses. Financial institutions are looking to bolster gender diversity initiatives. Many companies have now incorporated gender diversity efforts into their investment strategies.

For instance, the launch of Goldman Sachs’s GS initiative which aims to invest $500 million in gender-diverse companies and investment managers. Likewise, JP Morgan, in partnership with The Vinetta Project, recently launched an initiative to support women founders by providing them greater access to capital, networking opportunities, and advisory services.

The gloom view

There is also a view that the future is rather gloomy. With this additional compliance burden on European fintechs to work on their diversity in order to do an IPO and become a listed company, there is the cynical view that these companies could look to the U.S. or Asia and their less stringent frameworks in order to avoid doing the hard work. Or stay private for longer in order to somehow avoid scrutiny.

European fintechs are already looking to North America to go public, citing a deeper pool of investors as the main reason. Now, cherry on the fintech cake, it can also be a way to maintain the status quo by avoiding the governance and quotas imposed in Europe to get to a better diversity at the top of many organisations. That is not particularly far-fetched. It is not hard to imagine a column in the slide of a Board presentation listing “less stringent governance requirements” as a nice way to justify why a fintech company should go public outside of the EU.

What else can be done?

Given this gloom view of the world, it is quite certain that a lot can be done. But what, exactly? Depending on the stakeholders, a few things have to happen.

Fintechs

In order to ensure that they include female customers, fintechs must gather data on the gender makeup of their customer base. That is crucial: financial products made by men for men tend to have a natural bias and miss some important specifics. Among the 45 fintechs in the Inclusive Fintech 50 Benchmarks report, only 20 could report a number of female customers, indicating a data gap. This data will enable fintechs to track their contribution to female financial inclusion and identify areas for growth.

Women founders

Consider alternative sources of capital: Women are at an apparent disadvantage when it comes to traditional fundraising. But crowdfunding can be a very useful source of initial capital. Especially during times like this, when securing traditional funding may be increasingly challenging.

Women need to be highly visible to investors and network between each other. Industry associations and organisations can play a helpful role with this, both in underscoring the mandate for greater diversity in investment capital.

Investors

Providers of capital have a big role to play. For instance by improving networking access and welcoming women to venture capital firms. It is crucial to spread necessary funding support to early-stage fintech entrepreneurs of all sorts, not only led by men.

Investors need to widen the investment lens & actively avoid unconscious gender bias in the VC pitching process. A 2014 study by Harvard Business Review concluded that investors often make funding decisions based on gender. Furthermore, the study revealed that after listening to identical pitches given by men and women entrepreneurs, investors preferred pitches made by men.

Another study found that venture capitalists often posed different questions to men and women entrepreneurs. Men were more likely to be asked about the potential for gains, while questions toward women focused more on the potential for losses. Interestingly, this happened whether the investors were men or women.

Researchers

Research organisations can provide valuable evidence to build a case for investment in female-led fintechs and the nuanced barriers that female-led fintechs face. Research is a strong weapon in order to lobby governments and regulators. It forces public bodies to act and do something about gender imbalance and lack of diversity in companies. Building upon work by organisations such as Women’s World Banking, researchers can demonstrate that female-led fintechs produce strong financial returns while also making unique contributions to financial inclusion.

Additional research is needed to examine the challenges faced by female fintech founders.

Further research should examine the role of fintechs in serving women. Some questions to explore further can include:

- how to monitor the performance of fintechs;

- how to co-create products and solutions with female customers;

- effective marketing strategies to onboard women;

- the relationship between fintech and the SME credit gap;

- and whether credit scoring algorithms introduce gender bias

The world as a whole

Expanding visibility for female workers in the industry has the potential to spread awareness of their success stories and inspire rising female entrepreneurs to take a chance and get into the field.

Role models can play a huge role in driving positive change by inspiring other women to follow in their footsteps. For instance, success stories like the one of Dhivya Suryadevara in the U.S. has the potential to inspire thousands of women across the country but also globally.

Companies need to implement family-friendly policies. Work-life balance is not a gender issue but affects disproportionally women when work environments are rigid. The responsibilities of household life goes across genders. An “agile” working environment should be the goal of every organisation; one that flexes to support the needs and realities of employees in the digital age.